How to Choose the Best Health Insurance Plans in India?

To choose the best medical insurance in India, you must consider the below-mentioned advantages:

- Verify Eligibility: Often, health policies come with entry age restrictions. With Care Health Insurance, you face minimum age restrictions with a minimum entry age of 91 days on a floater basis and get lifelong renewability.

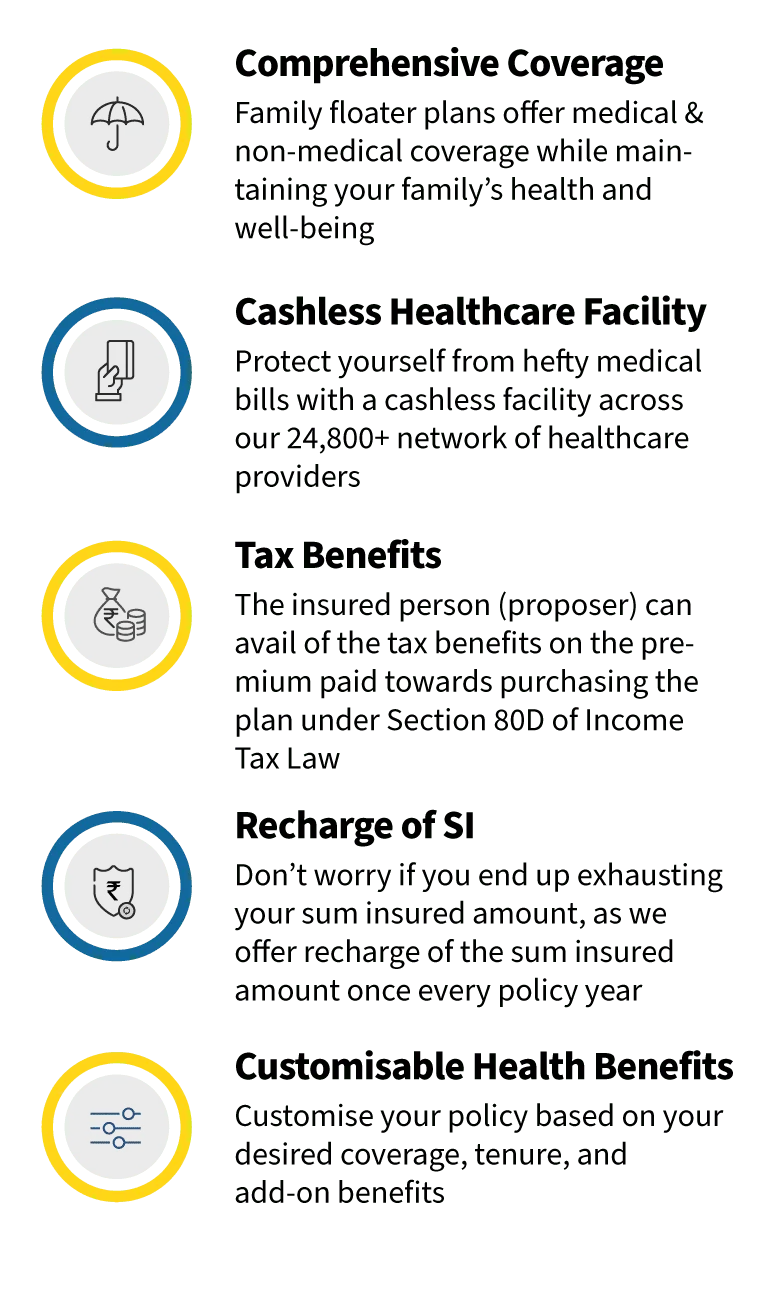

- Ensure Maximum Coverage: Our health insurance plans provide pre and post-hospitalization expenses, diagnosis expenses, treatment, medication, organ donor cover, and annual health check-ups.

- Look for Affordable Premium: A budget-friendly premium is always on your mind while buying a medical policy. In our digital portal, you can utilise the health policy calculator to estimate the premium rates by customising the covers and sum insured as per your needs.

- Check Exclusions: Check the exclusions list carefully before choosing a health policy. There are certain pre-defined conditions under which you cannot make a claim. So, go for the cover that offers maximum coverage with minimal exclusions.

- Understand the Co-Payment Clause: Before investing in insurance for medical needs, it's advisable to check the co-payment clause. Co-pay in health policies refers to a specified percentage of the claim amount that needs to be borne by the insured person.

- Select Wide Cashless Network Hospitals: Easy access to our empanelled network hospitals provide you with cashless treatment in the least time. Ensure a widespread cashless hospital network, and don't forget to look for well-renowned hospitals in your vicinity.

- Bid for Higher Claim Settlement Ratio: Claim Settlement Ratio proves the company's reliability in settling claims. We promise the highest claim settlement ratio of 95.2% CSR (F.Y. 19-20).

How to Buy Health Insurance Online?

The best part about the online availability of health covers is the secure payment gateways. With easy-to-follow steps and trust-backed payment partners, we offer you a seamless experience of buying the best health insurance plans in India completely online. Also, our digital portal enables you to effortlessly make premium payments through a hassle-free digital payment gateway. Welcome to the future of hassle-free health coverage with Care Health Insurance!

Here is a quick 6-step guide you should follow for making online insurance payments:

- Go to our home page and select a health policy based on your needs and sum insured requirements.

- Click on ‘Get Quote’ and provide relevant details.

- Enter the required information and customise your policy.

- You will be redirected to the payment section.

- Make payment through any secure digital payment mode.

- You will get the new health policy documents on your registered email-id.

How to Renew Health Insurance Policy Online?

Every medical policy terminates when the term for policy ends. That’s why renewing a mediclaim is crucial to ensure uninterrupted healthcare coverage and added advantages like no claim bonus, coverage for a pre-existing ailment, etc. The process of renewing insurance involves the following steps:

- Visit our official website for health insurance policy renewal.

- Go to the renew section.

- Enter the complete details, such as insurance policy number, contact number, etc.

- Under the payment section, pay the renewal premium through any secure payment mode.

By buying a health policy online, you can also renew your health plan digitally, thus saving much effort.

Advantages of Buying Health Insurance Online

Embrace the ease of securing your health online, with our digitally-enhanced portal. All you need to do is simply select your preferred health cover plans, fill up the details, and pay through secure transaction modes. Here’s why and how we ensure customer-friendly purchase a medical insurance plan online:

Chat Option for Queries

Our team is always available for all your queries concerning the terms and conditions of our healthcare policies. By accessing the live chat option, you can quickly discuss any policy-related matter at your convenience. No appointment is required.

Instant Premium Quote Calculation

We facilitate digital premium calculators to help you evaluate and opt for customised healthcare insurance for your family members.The ability to choose your desired health coverage and optional benefits helps us serve you the best mediclaim policies.

Secure Payment Modes

Our fortress-like secure payment gateways offer various digitally secure modes, including credit/debit cards or net banking. Once purchased, you will receive authentic policy documents immediately.This way, we help you get an instant mediclaim policy in less than an hour.

Transparent Policy Evaluation

What we promise on paper is what you get in times of emergencies. All our healthcare insurance plans include all the terms and conditions for your ready reference. Our commitment to transparency knows no bounds!

Readily Available Value Added Services

While browsing online through our mediclaim policies, you can easily check out other add-on benefits. These include OPD care, co-payment waiver, and reduced wait time for pre-existing diseases, among others, to cover your specific needs.

Helps Save Money

The offline method of buying mediclaim policies usually result in increased costs due to numerous factors like agent fees. Insurance agents get a commission for selling mediclaim policies , which increase the cost of the policy. Purchasing a health insurance plan online can help eliminate overhead expenses. Further, some insurance companies also offer an additional discount when you purchase plans using their online platform.

Some Myths about Health Insurance Busted

Health insurance is vital to financial planning, yet various misconceptions surround it. Let us examine the most common health insurance myths and help you understand what is a myth and what is not.

Health Insurance is only meant for seniors

It is a common myth that only seniors require health insurance to cover the medical expenses of age-related issues. Among younger people aged >50 years, the incidence of cardiovascular disease has been rising due to their poor lifestyle, deficiency of nutrients, and lack of exercise for calorie burn. Therefore, health insurance plans are vital for everyone. If you buy it at an early age, you won’t have to pay an expensive premium. You will be able to buy it at cheaper premium. health insurance plans may come with a waiting period against specified ailments. Thus, insuring your health and wealth is a wise choice to make at an early age.

You will be covered as soon as you buy the plan

While your coverage will start as soon as you buy a health insurance plan, you must first serve a waiting period. This is a 30-day period when a claim cannot be raised except for an accidental injury. When you buy a health insurance policy, you should enquire about your policy’s waiting period. For instance, coverage of certain treatments may require you to wait for a specified waiting period.

You should opt for the cheapest plan

Absolutely not! While the cheapest policy sure looks attractive, you should carefully think about why you want this plan and what benefits you expect from your plan. You should never make the prices the only criteria for choosing the plan. You might not be able to get the required benefits from your plan if it is cheap. Therefore, make sure that the plan that you have been buying is offering you comprehensive coverage for all your medical expenses.

I can’t buy health insurance if I have an illness

Having a pre-existing illness doesn’t make you ineligible to make a claim. Your insurer may ask you to serve a specific notice period before being eligible for the coverage, or you may ask for an additional premium or both.

Did you know? Health insurance plans such as Care Supreme even offer add-on benefits to reduce your Pre-existing disease waiting period for specified ailments!

Simply put, if you secure your pre-existing health condition with Care Supreme, you may reduce your waiting period by paying a slightly higher premium!

Group health insurance is enough

While it is a great perk to have corporate health insurance, you should not entirely depend on it. In most cases, a group plan will offer you limited coverage because its premium is deposited by your employer. You may lose all the accrued bonuses and other benefits when you change or leave your job. Furthermore, group health insurance might not be able to beat medical inflation. With a modest sum insured, you won’t be able to cover the medical expenses for critical illness and hospitalisation. Hence, consider buying an individual health insurance plan over and above the group coverage.

All my hospital bills will be covered

Despite a comprehensive plan, not all your bills will be covered by your insurer. Read the policy wording, and understand its terms and conditions. You need to know about exclusions, which are conditions that are not covered under your health insurance plan. Similarly, you should know about the co-payment clause of your insurer where you need to bear a part of the claim amount. Additionally, you can’t claim the uncovered expenses.

Porting Your Health Policy to Care Health Insurance

There are more than one reasons to port your policy to Care Health Insurance. As an insured person, we promise you unique benefits with lifelong renewability under most of our health insurance plans. Porting a medical plan is easy and can be done before the policy renewal stage. Just notify your existing insurer at least 45 days before the policy renewal date of an existing medical cover.

You will be able to retain your medical insurance policy benefits and accrued bonuses and transfer the time-bound exclusions, including credit for the waiting period for pre-existing diseases. It is possible to port a policy from one insurance company to another and from one health insurance policy to another policy with the same insurance company.

Things to Keep in Mind When Porting Health Insurance

When you port a health insurance policy to a new insurance provider, the aim is to get better services and coverage. Keeping in mind the following aspects will help you in a seamless transition.

Inform your previous insurer

Before switching to a new health insurer, it is vital to inform the current insurer. You should write an application for this purpose. You can make this request to your insurer at least 45 days before your policy’s expiry date. Also, keep in mind that you should avoid making this request before 60 days of the renewal. Let’s understand how to make the portability permission request. You should write an application in which you have to mention the name of your new insurer and other personal and details. Once you apply, your application will be reviewed and you will receive an acknowledgement within 3 business days.

Keep an eye on the premium

When you decide to port your health insurance policy to a new insurer, you should enquire about the premium. You should check whether its premium will increase or decline on porting. The change in premium indicates the changes in your coverage or benefits. So, gather this information before you finalise the porting.

Check for the available add-ons

If you are thinking of switching to a new insurer to enhance coverage or benefits, you should check for the available add-ons. You can buy the add-ons of your current insurer to avail of the extended benefits.

Understand the waiting period

You should understand the waiting period cycle before you port to a new insurer. Simply put, the waiting period is divided into three parts.

- The first waiting period starts with buying the policy. This is for only 30 days.

- The second waiting period is from 1 year to 2 years for the diseases of kidney stones and appendicitis.

- The third waiting period is 3-4 years, and it applies to pre-existing diseases. The good news is that when you switch to a new insurer, your waiting period does not start from the beginning. It starts where you left it with the previous insurer.

Suppose you have completed the waiting period of 2 years for a pre-existing disease that has a total waiting period of 3 years. Then, you need to complete the waiting period of only one year.

Give correct details about your medical health

Hiding your medical history when you make a porting request to the new insurer can be a mistake. Your new insurer may or may not make you undergo a medical test. In case you have been suffering from any chronic illness or severe comorbidities, your porting request may be rejected. Because in such medical cases, the threat of hospitalisation and the frequent visits to check-ups or treatment always persists.

Choose a higher sum insured

Obviously, you have decided to port to a new insurer because you are optimistic about new benefits there. Hence, you should try to choose a higher sum insured when you port.

Check Insurer Details

Before you decide to port your mediclaim policies to a new insurer, it might be a good idea to be aware of a few metrics. You should always check for details like discounts being offered, any consumer complaints, company’s empanelled network healthcare providers and the claim settlement ratio. It might also help to check the ratings on the company’s social media handles to understand the overall customer experience.